Why We Invested In Tori Finance

|

Can Gurel

At Delphi Ventures, we think about opportunities in crypto in two broad categories.

The first are products that could not exist without crypto: new forms of money, markets, coordination, identity, and ownership. The second are products that existed before crypto, but become dramatically better when rebuilt on open, transparent, programmable, and composable rails.

Our investment in Tori Finance falls squarely in the second category. Tori takes a portfolio of institutional, market-neutral yield strategies that already work offchain and rebuilds its access and utility around crypto rails.

Tori’s initial yield engine combines USD-hedged global money-market carry with complementary market-neutral arbitrage strategies. These strategies are not new. Hedge funds, sovereign wealth funds, pension funds, and large asset managers have long used hedged carry to capture global rate differentials while hedging out currency exposure. What is new is making that exposure accessible, liquid, transparent, and composable onchain.

Access to these strategies is typically gated by local banking relationships, broker access, high minimums, jurisdictional friction, and institutional-only fund structures. And even once invested, capital often remains locked. Investors may earn the underlying yield, but their positions sit in fund or brokerage accounts where they cannot move freely, be borrowed against, or plug into other financial applications.

Tori changes that by transforming a traditionally gated exposure into a tokenized, yield-bearing asset that can move freely across wallets and DeFi applications. Rather than sitting idle in a fund or brokerage account, strUSD can serve as collateral across lending markets, unlocking unprecedented capital efficiency.

Where does the yield come from?

Tori’s initial and main yield strategy is to take advantage of persistent inefficiencies in USD-hedged EM carry. It captures the interest-rate differential between currencies by gaining exposure to higher-yielding EM rates while hedging the currency risk back into USD.

In theory, the FX hedge should eliminate most of the spread. In practice, many EM markets are segmented, difficult to access, and shaped by local policy and liquidity constraints. The hedge side is also structurally uncrowded, because many local participants do not hedge their currency exposure.

As a result, the hedge reduces the gross local yield, but doesn’t necessarily eliminate it. A market can offer a very high nominal yield, and after paying for the FX hedge, still leave an attractive USD-denominated return.

Consistently capturing attractive yields in this market takes more than identifying a high-rate opportunity. It depends on direct market access, local accounts, strong execution relationships, competitive FX pricing, and sufficient volume to receive institutional terms. Without that infrastructure, much of the spread is lost to middlemen, prime brokers, and smaller OTC lines.

Operationally, Tori is built to preserve more of the underlying spread and make institutional-grade yield opportunities broadly accessible. Importantly, Tori doesn’t internalize every layer of trade execution to make this model work. Tori defines the strategy mandate, risk limits, and oversight framework, while established institutional trading desks handle execution, bringing decades of experience running similar strategies at scale and managing billions of dollars in volume.

The relevance of that preserved spread extends beyond simple yield access. RockawayX’s Tori Ecosystem Vault offers a useful reference point for the type of return profile strUSD is designed to target: its summary table lists a Phase 1 target of 8% real APY and 16.73% total APY, and a Phase 2 target of 10% real APY and 16.9% total APY, with points APY included in the total APY figures. These are targets, not guarantees. Realized returns may fall below them and as with any vault participation involve risks. But if strUSD’s recurring yield remains meaningfully above stablecoin borrowing costs, it can become useful not only as a savings product, but as productive collateral inside DeFi.

Looping Turns Yield Into Collateral Demand

This is where the spread matters. In lending markets, users can post strUSD as collateral, borrow stablecoins against it, and use those stablecoins to acquire more strUSD. As long as the yield on strUSD, generated by the underlying strategies, remains meaningfully above stablecoin borrowing costs, this process can be repeated in a loop to amplify returns on deposited capital.

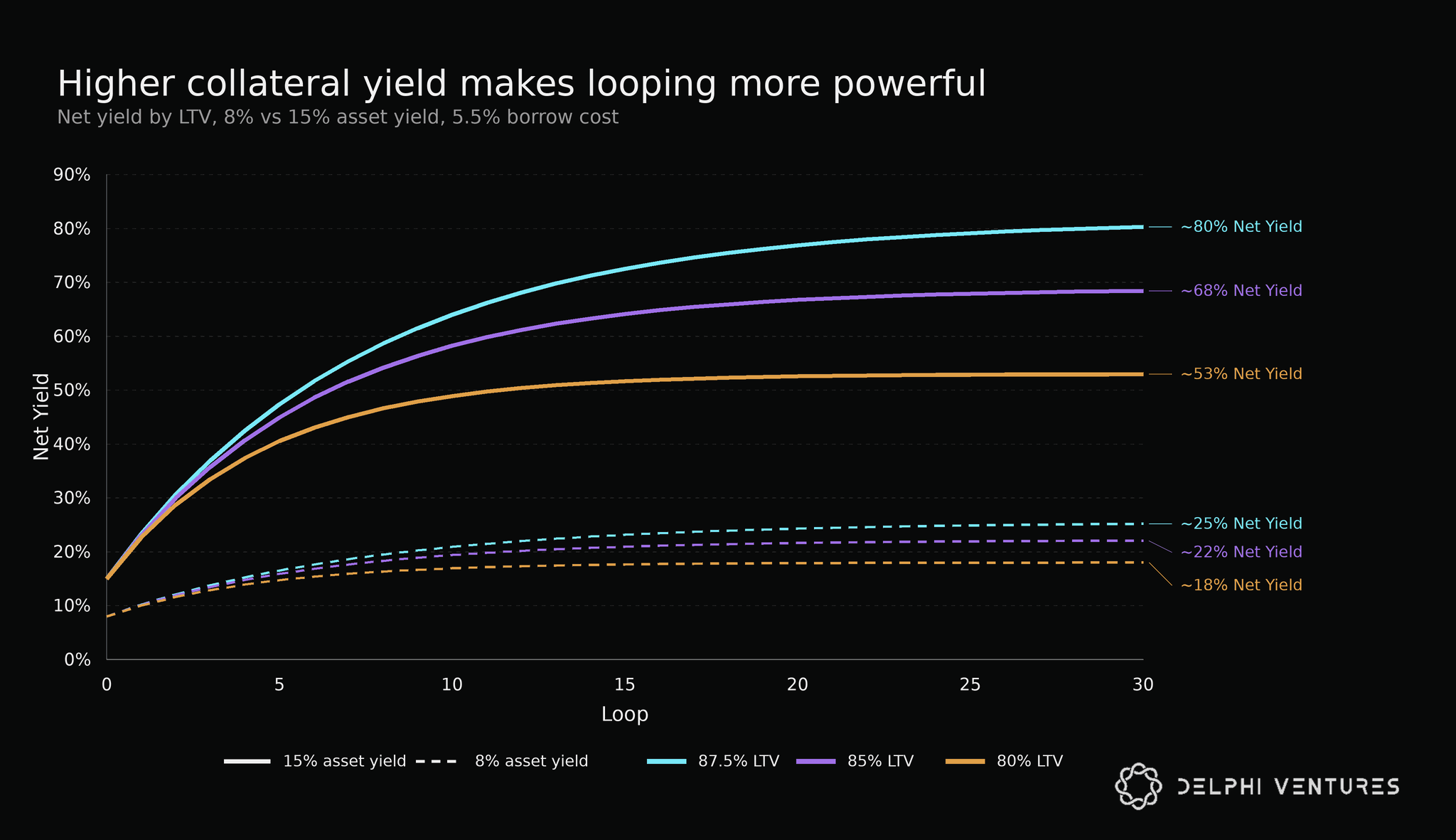

As a stylized illustration, if a user targets 85% LTV in a market with 91.5% LLTV, a 15% yielding collateral asset financed at a 5.5% borrow cost would generate roughly 69% annualized net return on equity at 6.67x gross leverage. This reflects earning 15% on 6.67x collateral exposure and paying 5.5% on 5.67x debt. The position has a 6.5 percentage point LTV buffer before liquidation, which corresponds to roughly a 7.1% collateral value drawdown if debt remains stable. This is illustrative and excludes fees, slippage, changes in asset yield or borrow rates, oracle effects, liquidity constraints, redemption frictions and other risks but the core point is simple: in traditional finance, this kind of leverage typically requires bespoke financing arrangements and institutional relationships; onchain, it can become a permissionless financial primitive that users access according to their own risk tolerance.

Looping has been a growth driver for yield bearing assets. But benefits don't accrue evenly across the category. When an asset yields 3.5–5% and stablecoin borrow rates are in the same range, there is little room for leverage to create attractive returns. After fees, utilization changes, slippage, and execution costs, the trade either does not work or works only temporarily.

The next chart illustrates why the same looping mechanics produce very different outcomes depending on the collateral yield. With a 5.5% stablecoin borrow cost, an 8% yielding asset leaves only a thin unlevered spread, so even at high LTVs, net yield plateaus around 18–25%. A 15% yielding asset is only 7 percentage points higher on an unlevered basis, but leverage magnifies that gap across the whole position: at the highest illustrated LTV, the difference expands to roughly 55 percentage points of levered net yield, or about 80% versus 25%. The curves flatten because each additional loop adds less incremental exposure than the last, but the takeaway is clear. Leverage only becomes powerful when collateral yield sits meaningfully above the cost of debt.

We already see implications of this in practice. Dune’s analysis of composable RWAs shows that higher-yielding credit and reinsurance products have become some of the most actively used forms of collateral, despite having far less AUM than tokenized Treasury products. A 3.5–5% Treasury product may be a strong savings instrument, but it is a weak looping asset. A 6%+ credit or reinsurance token has a better chance of becoming productive collateral.

Source: https://dune.com/queries/7477515/11424731

Collateral Quality Depends On Underwritable Risk, Not Yield Alone

The best collateral is not always the highest-yielding asset, or even the safest one. It is the asset whose risks can be understood, monitored, and priced by curators and lenders. The question is not just whether the yield is high but whether it is durable, whether the NAV is stable and transparent, and whether the redemption path is predictable enough for lending markets to evaluate the asset as collateral.

Tori’s base return drivers — monetary policy, local market structure, FX forwards, hedging demand, and execution pricing — tend to move more slowly and observably than crypto-native APYs driven by incentives, borrow demand, or funding rates. The yield is not guaranteed, and the spread can compress, but drawdowns are generally easier to monitor, price, and underwrite.

This is important because a levered looping strategy only works as long as the spread remains positive. If spread compresses, users need a predictable path to de-lever. That unwind process takes longer for RWAs than for crypto-native collateral because offchain positions involve settlement, counterparties, and liquidity management. Tori is not immune to these constraints. strUSD has a seven-day cooldown to account for the mismatch between onchain actions and offchain operations. This is slower than unwinding crypto-native collateral, but far more workable than the monthly, quarterly, or bespoke redemption windows that many more exotic exposures require.

The broader market is also building around this challenge. Protocols like 3F are developing financing infrastructure that makes it easier to assemble and unwind levered RWA positions. We agree with Sonya Kim of 3F that over time, RWA leverage should look less like manual DeFi looping and more like an onchain prime brokerage network, where financing, liquidity, and collateral operations are coordinated by specialized markets.

Fixed-rate lending is another important tailwind. Most DeFi borrowing today is floating-rate, creating uncertainty for leveraged yield strategies. As fixed-rate and fixed-term markets mature — through initiatives like Morpho’s Midnight — users will be able to lock in financing costs against yield-bearing collateral, making leveraged RWA strategies easier to structure and underwrite.

Transparency is the other side of the same equation. Users and institutions increasingly expect visibility into how yield is generated and what risks sit beneath it. After 2022’s collapses, they are far more diligent about understanding where returns come from, who holds the assets, how NAV is calculated, how hedges are executed, what happens in stress, and how redemptions work.

RWA yield is not a single category. Credit, reinsurance, GPU loans, trade receivables, tokenized Treasuries, and EM carry all sit under the same broad umbrella, but each comes with a different risk profile across counterparty exposure, liquidity, FX hedging, NAV and oracle design, smart contracts, operations, and regulation. The winners in this category will not be the teams that promise the highest APY or the safest asset. They will be the teams that make risk visible enough for users, curators, and institutions to underwrite.

Tori is building with that standard in mind. A key part of its transparency stack is Accountable, which is emerging as one of the industry's standard verification layers for offchain yield sources.

At a high level, Accountable connects to custodians, exchanges, banks, brokers, and onchain wallets to monitor assets, liabilities, exposures, and NAV from the underlying sources of truth. The goal is to move beyond issuer-reported balances, static audits, or manually uploaded snapshots, and toward continuous verification of the data that matters for users, curators, lending markets, and institutions. To reinforce that verification layer, Tori is also working toward regular third-party attestations, potentially weekly or monthly, to confirm that the Accountable dashboard matches the actual underlying positions.

RockawayX’s Tori Ecosystem Vault shows how this transparency stack can plug into the curator-led model already emerging across DeFi lending. Accountable provides independent verification of assets, liabilities, and NAV, while RockawayX uses that data to support curation, risk monitoring, and allocation decisions within a governed vault policy. The result is a clearer division of labor: verification layers make offchain collateral legible, and curators translate that information into the risk parameters, exposure limits, and allocation decisions that lending markets need. Together, these layers make new forms of RWA more scalable across DeFi.

Why Now?

That is what makes the timing important. The underlying strategies are not new, but the infrastructure required to turn them into liquid, transparent, composable collateral has only recently come together.

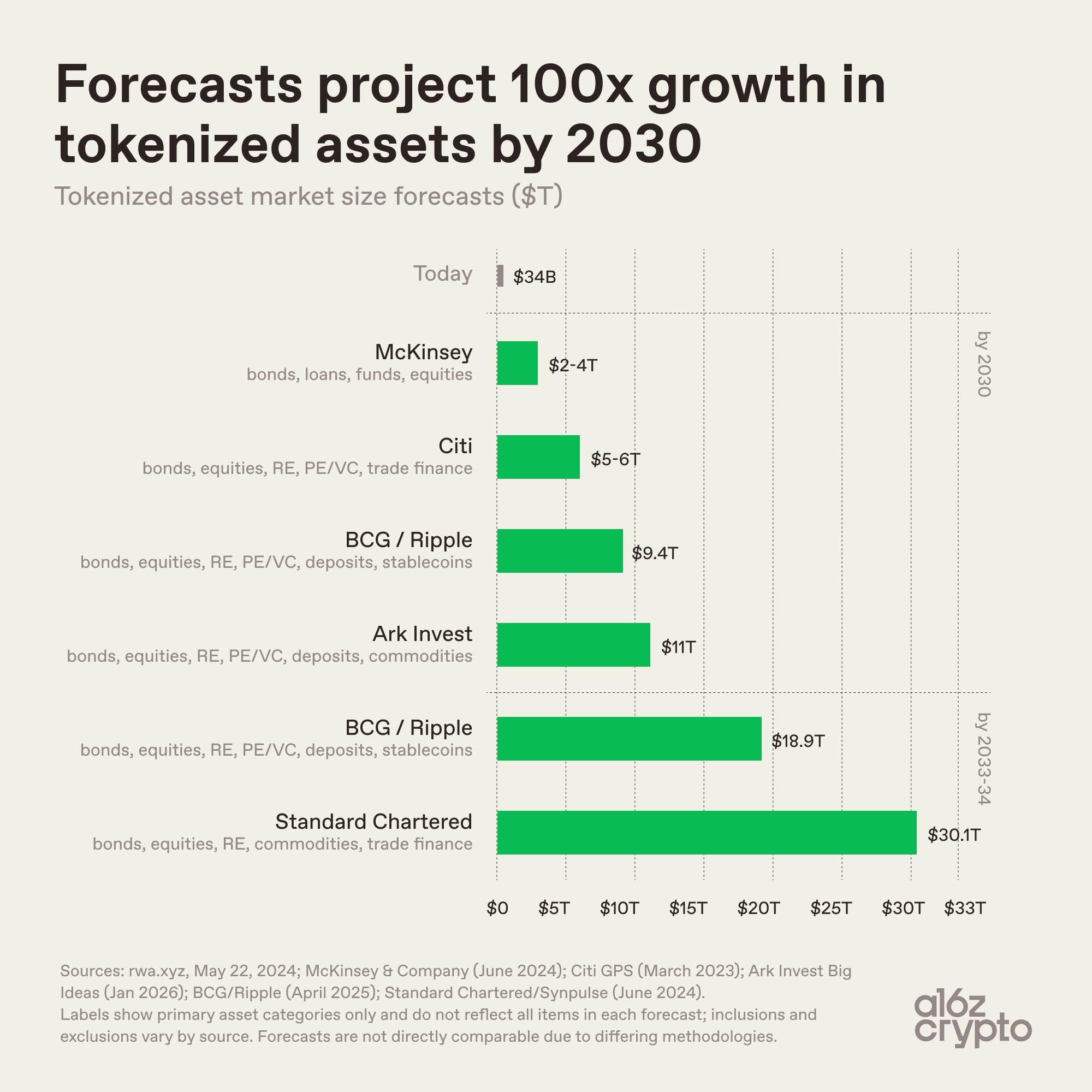

Five years ago, the underlying strategy could have existed, but the surrounding infrastructure would not have been ready. Today, the pieces are coming together. Stablecoins have become the settlement layer of crypto, growing from roughly $25–30 billion in supply in 2020 to more than $330 billion today. Tokenized RWAs have followed a similar trajectory, expanding from a niche category into a market with approximately $34 billion in onchain assets within two years.

At the same time, lending markets are becoming more modular, curators are underwriting bespoke collateral, and NAV oracles, proof-of-reserve systems, fixed-rate lending, vault and RWA unwind infrastructure are all maturing in parallel. This mirrors Pantera’s State of Tokenization framework, which argues that the next phase of tokenization will be measured less by whether assets are represented onchain and more by whether they become programmable, composable, and actively used in DeFi. Together, these developments are creating the foundation for a new generation of yield-bearing, composable financial assets.

Ethena is the clearest proof that demand is here. It taught the market how to think about yield-bearing synthetic dollars and scaled the category from an idea into one of DeFi’s most important products. We are investors in Ethena and remain highly convicted in its role as core synthetic dollar protocol. Its recent partnerships with Coinbase and Janus Henderson further show the category is heading towards broader distribution, more institutional backing, and more diversified yield sources.

Tori builds in that same direction, but from a different starting point. Instead of crypto-native basis as the primary engine, Tori brings USD-hedged global money-market carry and market-neutral arbitrage onchain.

Source: https://a16zcrypto.com/posts/article/tokenized-asset-rwa-market-data-charts/

Why Sam and the Tori team?

Sam has the kind of intensity, technical depth, and high agency we look for in early-stage founders.

He is a technical entrepreneur who began coding at age 10 and has been building products ever since. He grew up in Istanbul, studied computer science at one of Turkey’s top universities, and graduated second in his class while freelancing as a software developer for global customers including Dior, LVMH, Chanel, L’Oreal. He later built, scaled, and exited his SaaS startup to BTC Turk, the largest crypto exchange in Turkiye.

After the exit, Sam lived the user side of yield-bearing stablecoins. He spent years as a DeFi allocator, farmer, angel investor, and early participant in many of the protocols that shaped the market. In practice, his “retirement” looked less like stepping back and more like full-time market immersion. He came out of that period with a clear view of how stablecoin capital actually moves onchain, what users care about, where incentives work and why DeFi needs more durable offchain yield.

Tori’s success depends on turning that insight into repeatable execution across fragmented offchain markets and jurisdictions. That means opening local accounts, building banking and trading relationships, securing institutional FX execution, managing counterparties, and continuously sourcing, hedging, and monitoring opportunities across markets where access itself is part of the edge.

This is where Sam and the team’s high-agency operating style has strong founder-market fit. Pre-launch, they have already pushed through multiple institutional diligence processes: QInvest serves as Tori’s main execution partner, bringing an institutional trading desk that already manages and trades billions of dollars across relevant markets; RockawayX is an anchor LP; and Nexus Mutual is offering insurance on a pre-live product. These are early signs that the team can assemble the institutional relationships and operating stack required to make the strategy scalable and underwritable. We believe Sam and the Tori team have the founder-market fit and execution edge to build one of the defining products in this category.

Over time, Tori can deepen direct access and broaden the strategy set. But the core opportunity is already clear. Tori is turning difficult-to-access offchain yield into transparent, USD-denominated, productive collateral for DeFi. That is what makes the product powerful. Not just the yield itself, but what crypto rails allow users and markets to do with it.

Important Disclosures

Delphi Ventures (“Delphi”) is an investor in Tori Finance. Delphi is also an investor in Ethena, which is referenced in this post. This post is for informational purposes only, reflects the views of Delphi as of the date of this publication, and does not constitute investment advice or an offer to buy or sell any security or investment product. Yield figures and return illustrations referenced herein are targets or hypothetical examples only and are not projections or guarantees of future performance. Actual results may differ materially. Forward-looking statements are subject to risks and uncertainties. This post has not be reviewed or approved by any regulatory authority.